- Ghosh Capital

- Posts

- Don't Call It a Comeback: Q2 2025 Letter

Don't Call It a Comeback: Q2 2025 Letter

Shomik Ghosh

July 01, 2025

Q2 2025 marks a special quarter as it’s officially 1 year since inception of this account and these letters (back catalog here). In that time, we had the drawdown in July-Aug 2024, Pre Inauguration Chop, Deepseek Selloff, Tariff Decline, V-Shaped Rally, and Geopolitical turbulence all along the way. What a year!

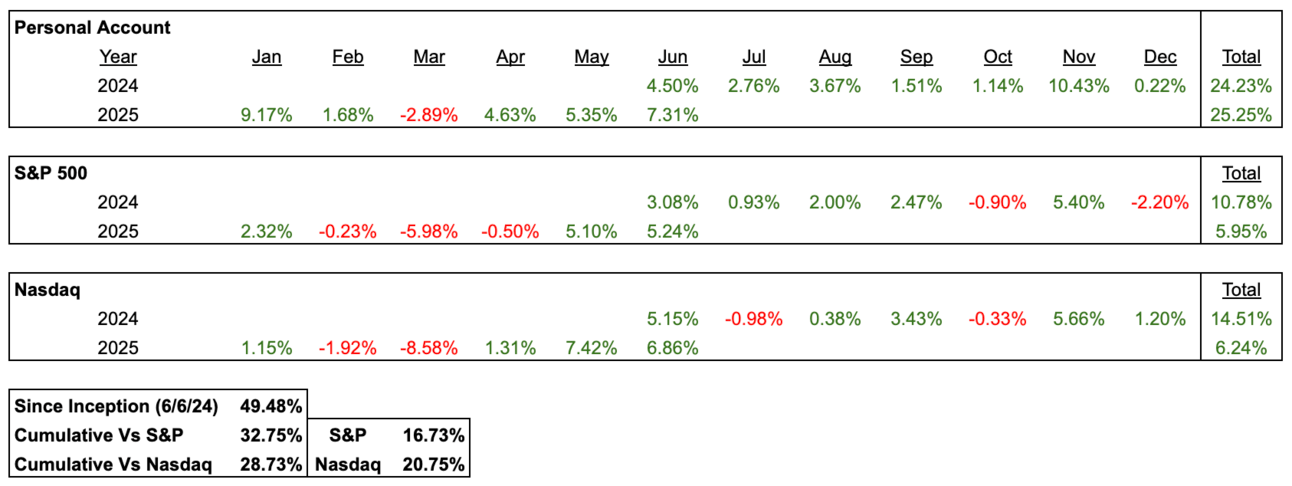

Since June 6, 2024 (inception), the portfolio returned 49.5% vs S&P 500 at 16.7% and Nasdaq at 20.8% (monthly performance table at end of the letter as always).

For Q2, the portfolio returned 17.3% vs S&P 500 at 9.8% and Nasdaq at 15.6%.

YTD, the portfolio returned 25.3% vs S&P 500 at 6.0% and Nasdaq at 6.2%.

Stretched Valuations Guiding Opportunity Capture

Q2 2025 continued the trend of being a great stock-pickers market. Part of what allowed the portfolio to be resilient during the Tariff selloff was lightening up in February (at one point in nearly 50% cash) due to sector valuations that looked quite high even though individual positions in the portfolio still looked relatively attractive when looking at comps. That enabled cash to be put to work at the bottom along with observing a spiking VIX signaling high levels of fear, early signs that tariffs were in fact a negotiating tactic to make deals and not a hard line, and attractive valuations in many companies.

Large positions in Microsoft, Mercado Libre, Rheinmettal, Robinhood, Broadcom, and Amphenol at or near the lows on April 7 allowed some good upside capture as the market started to climb the wall of worry back.

Rest of the World Valuations

As discussed in last quarter’s letter, President Trump’s tariff strategy was actually a boon for equity markets around the world as investors discovered that attractive opportunities did exist outside the US.

Topicus, a spinoff from Constellation Software had deployed FCF at a rapid cadence into acquisitions and investments in Q1, a cadence that hadn’t been since from the team in all of 2024. And yet the stock didn’t move at all until post liberation day. The whole premise of Topicus is that they will deploy capital for inorganic growth at high ROICs. It went on to have a 40%+ return at its peak for a fairly widely followed stock that was trading >4% FCF Yield with durable high teens growth.

MercadoLibre sported a 7.5% FCF yield with mid 30% growth and was getting sold off…even though it wasn’t exposed to US tariffs!

At one point, the portfolio looked more like the MSCI All Country World Index vs anything resembling the Nasdaq or S&P 500. This did not come from top-down hunting for macro themes. But rather bottoms up focus on valuation discrepancies in high quality businesses and figuring at some point those discrepancies would be corrected.

The search for attractive valuations in high quality companies brought me to all parts of the world but particularly Canada (Kneat, MDA Space, Topicus) and Brazil (MercadoLibre, NuBank).

Current Top Positions

Kneat continues to be the top holding and I am thankful that I have gotten chances to add to it in recent months at 8x ARR even as the business proves out more of the platform, distribution, and industry sector story. It’s a high quality vertical SaaS business that would likely trade at 2x the valuation if it was on US exchanges or a private company. In the next letter, I will do a deep dive on Kneat.

Google is the #2 position. For those who have read these letters from inception, you will remember Google being 35% of the portfolio around the time after the botched Gemini release, Google “woke culture”, and Perplexity raising rounds killing Google narrative. It was the classic Silicon Valley Filter Bubble at work. And yet, somehow we find ourselves back here again a year later. AI mode is being ignored by investors even though it is creating delightful experiences for everyday users who’ve never accessed ChatGPT before (not just boomers but also people like my sister in law who works in healthcare). The Google 2.0 bull case is outlined in the tweet post below in short soundbites and to read the whole thread click here.

I keep getting sucked back into Google as the market delivers attractive opportunities

The 3rd biggest position is MDA Space, 4th is MercadoLibre, and 5th is Visa (a recent addition on misguided stablecoin fears resulting in a pullback but unlikely to be a long term hold not because of business quality but just expected IRR in longer term). For anyone who would like to chat stablecoins’ impact on the payments ecosystem, please reach out!

MDA Space

As always I like to do a deep dive at the end of these letters as a way of surfacing undiscovered names or variant perceptions to you all.

Since my first investment in March 2025, MDA Space is up 70% and yet it is only just beginning in my opinion. I have added to my position as recently as June.

Overview

MDA Space started in 1969 in Vancouver, that is 56 years of innovating in space from before SpaceX existed. Since that time, the company traded hands across various companies and private investors all the while accomplishing amazing feats such as building the Canadarm for the Internation Space Station and building many satellites mostly in GEO (Geostationary Earth Orbit) as pre SpaceX, launch costs were so high that it made sense to build a bigger satellite to cover as many use cases as possible.

MDA Space’s revenue comprises of building, deploying and maintaining satellite systems (60% of revenue), space robotics (24% of revenue), and Geointelligence (16% of revenue). Given it’s long history of successfully building satellites, it is trusted by governments, defense, and communication companies around the world. The majority of revenue today comes from Canada and the USA but as more countries look to build up their own space comms networks for defense and national use cases, MDA Space stands to benefit.

MDA Space has blue chip customers like the Canadian government, US government, UK Space Agency, Thales (France), Airbus (Europe), Boeing, Lockheed Martin, Telesat, and Globalstar (Apple being the end customer). The company is forecasting growth of 45% YoY, ramping up capex in order to build world class robotic enabled facilities to continue building state of the art satellites and space robotics, and is actually profitable. To make it easy for comparison at $3B EV MDA Space trades at 2.4x NTM Sales and 12.3x NTM EBITDA. Rocket Lab at $17B EV trades at 26.7x NTM Sales with no FWD EBITDA, AST SpaceMobile at $12B EV trades at 144.0x NTM Sales with no FWD EBITDA.

In MDA Space, you have a best of breed satellite and space robotics company with the longest operating history in the public company space but because it trades on the Canadian exchange exhibits a steep discount to US Space peers who have less revenue and similar growth.

Management

Mike Greenley, CEO of MDA Space has extensive experience in the defense tech ecosystem spanning 21 years across CAE, General Dynamics, L3 Technologies, and MDA Space. In his time he has led organizations building sensors, simulation software, military communications, and imaging analytics. All of these are aligned with MDA Space’s key business segments and certainly with the end customers.

Cameron Owner, CTO of MDA Space has been at the business for 26 years spanning a career across the space control center, systems engineering, and robotics & automation. He has touched every aspect of the R&D function in his career.

The Board of Directors is filled with experience across Space, Defense, and Government but one person that’s worth calling out in particular is Darren Farber, former US Deputy Under Secretary of Defense. For those interested in learning more about the defense industry, Invest Like The Best interviewed Darren in April 2025.

Business

MDA Space is one of the oldest and trusted manufacturers of space equipment. Three generations of their RADARSAT GEO satellites have been operating successfully since 1995. MDA’s robotic arms have been on the Mars Rovers since 2008 and MDA’s Canadarm has been on the ISS since 2001.

MDA Space currently manufactures mostly MEO and LEO satellites (60% of rev). The reason for this is with modern space launches, larger constellations of these two types of satellites can be launched vs GEO satellites are typically much larger in size. While the capability of GEO satellites is vast, MEO & LEO satellites are perfect for a larger communication surface area, frequent imaging, and just generally having more satellites in space. Major drivers of Backlog growth continue to be large constellation wins. Globalstar (servicing Apple’s mobile network) and Telesat are the largest wins in recent years. Echostar also plans to launch a constellation and is expected to choose MDA Space as their provider. More government wins are expected and in Q1 2025, MDA Space added another $750M to backlog. For context, SpaceX is building Starlink, Amazon is building Kuiper, and then MDA Space are building Globalstar and Telesat constellations. There are no other major commercial constellations announced outside of Rocket Lab saying they may start to build one in the future.

MDA Space develops space robotics, rovers and sensors (24% of rev). Notably the Canadarm was developed by MDA Space and to this day is still used by the International Space Station to make robotic adjustments to the station and equipment given the risks everything of having an astronaut going into space and doing it themselves. Canadarm 3 is a big robotics project that the Canadian Space Agency has granted to MDA Space. This is supposed to be attached to the Lunar Gateway, the new International Space Station. However, with proposed NASA budget costs this could be at risk in 2026 or beyond. The risk is mitigated though by the fact that the ISS is a core feat not only of engineering but collaboration between many different countries and it seems unlikely that the US would pull away from that.

At 16% of rev, MDA Space provides Geointelligence. This is analytics, imaging, and data from satellites used for everything from climate to defense to hedge funds. Of note, anytime MDA Space launches more satellites, Geointelligence benefits with a lag. The reason being, you can’t sell more analytics if you don’t have the satellites in space to provide them. So Geointelligence is a bit of a lagging revenue generator. So when MDA Space is in scaling mode, margins will look lower than steady state as development of the satellites is hitting before the software and data revenue comes in.

One final thing to note, is a lot of what MDA Space builds hardware wise is “recurring” in nature. LEO satellites burn up fairly quickly being close to the earth’s atmosphere or even just having wear & tear from space debris. MDA Space is also advancing the technology of satellites at a rapid pace and so you have a 5-6 year refresh cycle from wanting to get new tech up into space and also needing to replace the previous satellites to maintain connectivity.

Competitive Positioning

SpaceX and Amazon are competitors (although ironically Blue Origin is a customer of MDA Space). However, each are building constellations for their own use cases while MDA is a standalone trusted provider to anyone who wants to launch a satellite. Given geopolitical dynamics, governments, corporations, and defense industries around the world are wondering if they should entrust their space systems to anyone company. This bodes well for MDA as they already work with European countries and corporations.

Furthermore, a potential risk would be if one day SpaceX said they would refuse to put other satellite payloads up into space. This would be counter to SpaceX’s business model as while Starlink is definitely a huge current and future revenue generator, payloads and utilization of the rockets is core to making each launch exhibit compelling economics. As the cost curve for launches continues to decrease, MDA Space will continue to benefit from increased demand and better margins.

Reason to Own

There are very few opportunities to own a leading and trusted manufacturer of critical technologies with high barriers to entry at a cheap valuation. MDA Space hits all that criteria. They have massive tailwinds that should continue to reflect high growth for many years to come. They continue to push the satellite industry forward by developing new technology and have a proven and demonstrated track record of delivering durable systems for over 55 years. Package that up with a valuation that is meaningfully cheaper than peers and MDA Space represents a highly compelling high growth, tech advantaged investment opportunity.

NotebookLM Podcast

To listen to NotebookLM synthesize the Investor Presentation and recent earnings presentations click here: https://notebooklm.google.com/notebook/935ee015-26bf-4b61-83c1-23213b7eb216/audio

Monthly Performance