- Ghosh Capital

- Posts

- Lessons in Concentration & Leverage: Q4 2025 Letter

Lessons in Concentration & Leverage: Q4 2025 Letter

Shomik Ghosh

January 07, 2026

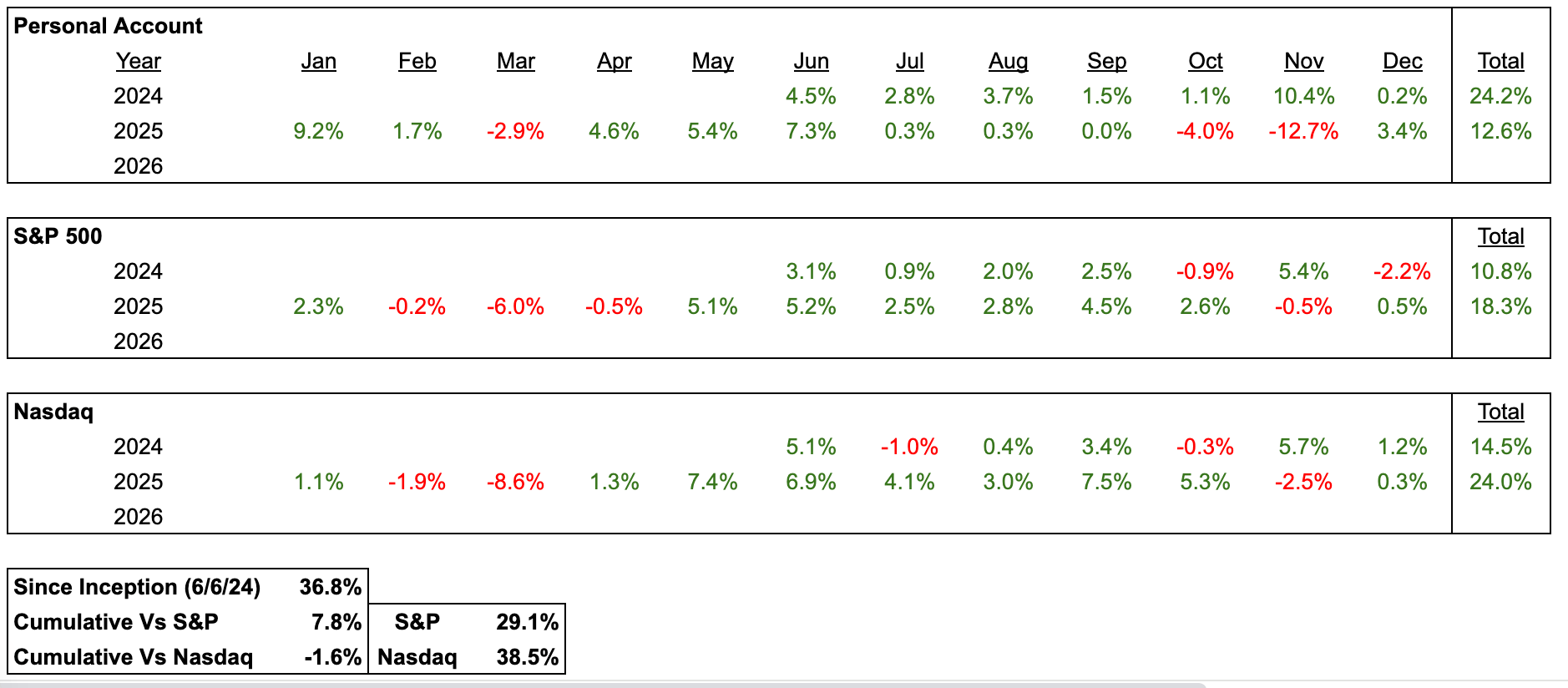

Since June 6, 2024 (inception), the portfolio returned 36.8% vs S&P 500 at 29.1% and Nasdaq at 38.5% (monthly performance table at end of the letter as always).

For Q4, the portfolio returned -13.3% vs S&P 500 at 2.6% and Nasdaq at 3.2%.

For 2025, the portfolio returned 12.6% vs S&P 500 at 18.3% and Nasdaq at 24.0%.

Frustrating Performance in Q4

Q4 was a gut punch to the outperformance that the portfolio was experiencing. From being up 50% in Q2 since inception to 37% while the S&P 500 and Nasdaq both increased substantially caused me to fall behind the indices for the year.

I definitely over-traded as I felt markets and valuations were getting frothy and also reached for stocks where I didn’t have high conviction but thought the markets were undervaluing the equity given how I felt everywhere else was overvalued.

The largest contributor to the negative performance was my concentration in Kneat at 30% of the portfolio. Kneat had rough Q2 and Q3 results where net new ARR added came in well below expectations as a result of macro and deals being pushed out. A 35% drawdown led prices to where I had first started accumulating in 2024.

My take away here is on position sizing. No matter how high my conviction is, I need to figure out what I would be ok with on max exposure and trim to manage risk around that. I still have conviction in Kneat’s long term prospects and think 2026 will see the stock price recover significantly as Kneat marches towards $90M ARR with a current enterprise value of $450M. Given the blue chip customer base, strong gross and net retention, and improving cash flow, Kneat continues to be significantly undervalued. 2025 ended with the highest number of new strategic customer wins in the company’s history which bodes well for 2026 and beyond given the cost of these wins lands on the P&L now with a smaller revenue land (typically $100k contract) to offset those costs. However, Kneat has historically expanded customers significantly after the initial land (Merck is now $3M ARR+ after having started at $100k) and so what looks like lower growth in 2025 is setting up for sustained higher growth in 2026 and 2027.

Options Leverage

Coming off of several large contrarian bets that played out well like Google, Micron, Nvidia/Broadcom during Deepseek selloff, aggressively adding at the April lows during the tariff selloff, I was feeling good about buying stocks out of favor by the market and started to reach into more speculative areas. I compounded this by being overconfident and taking on long-dated options positions in these companies. Wix and Clearwater Analytics were the two offenders here.

In neither of them, did I have very high conviction on the business models. I just thought they were too cheap for assets the market was missing. With Clearwater, the market was overly focused on the debt and large acquisitions while missing how core Clearwater was growing strongly still and had a tailwind from rate cuts. Wix had bought Base44 which was becoming one of the fastest growing $0-100M ARR “vibe-coding” apps. While Lovable, Replit and others kept getting higher valuations in the private markets, Wix was trading at a 6% FCF yield and had an AI native asset that was growing like a weed. Instead of going into common equity positions, I decided to buy deep in the money long-dated options to get more “juice” on the positions. While this may have worked well on names I know well and have studied for a long period of time, Wix and Clearwater Analytics were recent deep dives that I did over 1-2 months time. Clearwater Analytics ended getting bought out and would’ve netted me a large gain but in the meantime due to the size of the position I took and the options leverage, the weak performance was causing me to question my conviction until I decided to sell my position for a 30% loss, 2 weeks before the buyout news came through. On Wix, I just completely misjudged how the market would look at the outperformance of Base44 (gross margins are getting hit because running AI models without optimizing them for cost is lower than software margins). Because of the position sizing and options position, I once again sold for a loss rather than re-assess my position as the risk of total loss was too large for me.

Learnings Going Forward

Strict rules around max position sizing

Do not go “down the quality” spectrum to hunt for cheap names if can’t find opportunities in companies I know well

Use options sparingly even if deep in the money and far out in time as the inherent leverage can make it hard to hold onto positions

Contrarian calls have been right but unless the above is followed, there will be no way for me to see these calls through

Winners

I’ll keep this section short since my underperformance in 2025 is more something for me to correct than celebrate winners. My biggest gains came from Google, Robinhood, Amphenol, Microsoft, Rheinmettal, Sprott, and Agnico Eagle (the last two are precious metals positions that were small position sizes but delivered outsized returns given the performance of Gold and Silver in the quarter).

Monthly Performance

Deep Dive

I will hold my deep dive on a specific company for another letter. However, for those interested in hearing my Clearwater Analytics thesis, Andrew Walker had me on the Yet Another Value Podcast to talk publicly about it. With the buyout news pending, it has risen 30%+ in 3 months. Alas, I did not participate in any of the upside due to what I discussed above in the letter.